Climate risks fuel insurance costs, squeezing US households even inland / Photo: © AFP

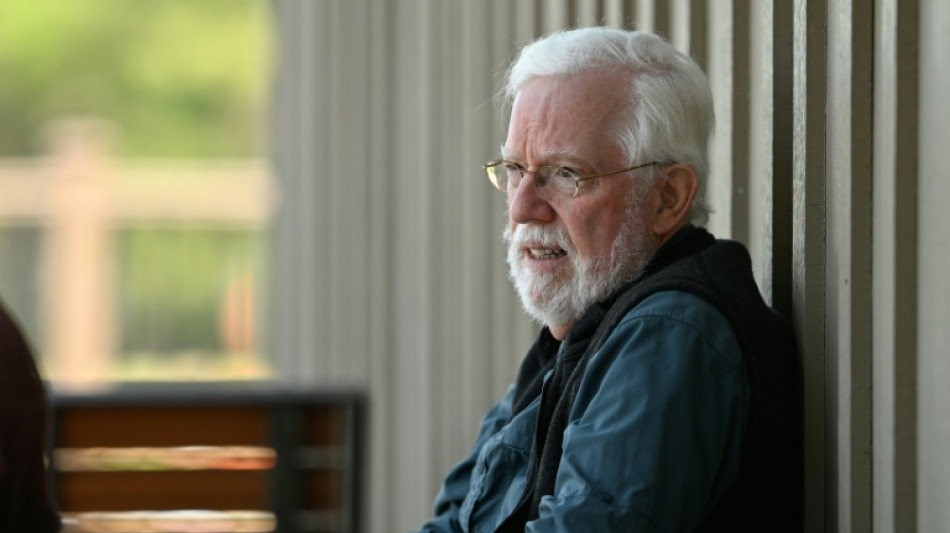

After Tony Dunn lost his home in a California wildfire, he moved to mountainous North Carolina to avoid more climate disasters. But his neighborhood was devastated in a hurricane six years later -- and insurance costs are climbing.

He is among a growing number of US homeowners feeling the pinch from insurance as disasters linked to climate change reach them more frequently, even away from the coast.

Dunn, 69, counts himself as lucky that his new home was not damaged in Hurricane Helene as his neighborhood was wrecked.

But that has not stopped his homeowners' insurance premiums from surging almost 30 percent to nearly $4,400 a year since Helene in 2024.

"It was a bit of a shock when we got the insurance bill last year," Dunn told AFP.

He worries about further increases but said: "As much as it costs, you don't want to be without insurance."

After he and his wife lost their home in the 2018 California Camp Fire, which claimed 85 lives, insurance payouts helped them rebuild their lives.

While coastal states like Florida have tended to face the worst of price hikes, inland areas have also seen costs rise in recent years following hail storms, wind damage and other disasters.

Climate change is enhancing conditions conducive to the most powerful hurricanes and it intensified Helene, a study by the World Weather Attribution scientists network found in 2024.

In Henderson County, where Dunn lives, homeowners paid an average of $1,979 for insurance in 2024, an 86-percent surge from 2018.

Nationally, rates skyrocketed 58 percent over the same period, according to researchers Benjamin Keys and Philip Mulder, who led a study released last year.

The hit to premiums tend to be larger in areas facing growing climate risk.

Dunn worries about people who forgo insurance coverage as costs rise.

"They're going to have nothing," he said. "Something needs to be done."

- 'A shock' -

Inland states like Iowa and Nebraska have also seen sharp cost hikes as climate risks mount.

Rates in Nebraska jumped 20 percent between 2023 and 2025, while those of hail-prone Iowa were up 54 percent, according to Insurify.

A 2025 working paper involving researchers from Columbia Business School, Harvard Business School and others found the average US household "under-insured at mortgage origination, with only 70 percent of the rebuilding costs covered by the insurance contract."

"We are increasingly inching towards a situation where insurers would need to charge much higher prices because climate risk is going up," said Ishita Sen, one of the researchers behind the paper.

But households' willingness are "not catching up," partly due to financial constraints.

Dee Dee Buckner in Marshall, North Carolina, told AFP she has considered doing away with homeowners' insurance.

"If they go up any higher, I can't," said the 60-year-old.

Buckner lost her home during Helene when the French Broad River swelled and flooded downtown Marshall with over 12 feet (3.7 meters) of water.

"There's been rain from hurricanes that's come in here before, but nothing of this magnitude ever. It was just a shock to everyone," she said.

- 'Climate epiphany' -

Since Helene, Buckner said she could only afford a "cheap little policy" for homeowners' insurance.

But she worries it will not cover much loss if disaster struck again.

Her flood insurance -- which is separate -- now costs $600 more annually and is up to more than $1,700.

Most US homeowners insurance does not cover flood damage, meaning households end up buying a separate policy if they face flood risks.

Keys and Mulder said in their earlier study that reinsurance -- insurers themselves buying protection against risk -- has bumped up premiums as firms experienced a "climate epiphany."

Construction cost inflation and other issues are also pushing up premiums.

But climate "is the most important structural factor," said research economist Sarah Dickerson of the Kenan Institute of Private Enterprise, a think tank.

The North Carolina Rate Bureau, which represents firms that write insurance policies, said it was the single biggest factor driving rate increases.

There are also indirect effects as insurers drop customers in hurricane-prone areas or withdraw from states. That could lower competition and lead to price changes too.

Dickerson calls it a "misnomer" to dub areas low-risk: "Climate-related losses are impacting all parts of the state."

S.Wilson--ThChM